For-profit college dropouts most likely to default on student loans

Dropping out of a college, in general, makes borrowers more likely to default on their student loans, because it makes it more difficult for them to find a good-paying job and afford their student loan payments.

But certain college dropouts have it worse than others–those who dropped out of a for-profit, less-than-four-year college.

High default rates for for-profit college students

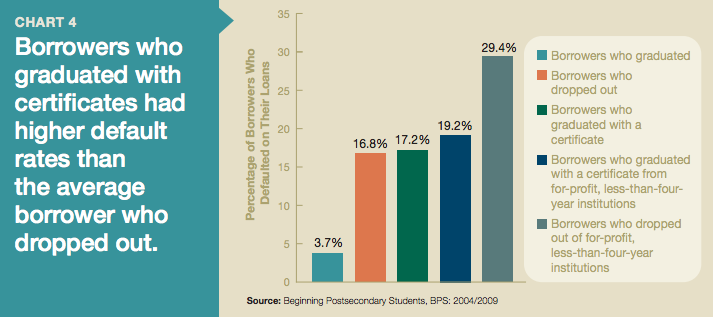

A study from Education Sector found that nearly 30% of these borrowers defaulted on their student loans–almost twice as high as the 16.8% of borrowers from all colleges who dropped out.

And they’re significantly more likely to default than college graduates in general, with only 3.7% of these borrowers defaulting.

Students who dropped out of a less-than-four year for-profit college were most likely to default on their student loans, followed by graduates of these colleges.

What’s even more interesting is that even students who graduated with certificates from these less-than-four-year for-profit institutions were more likely to default on their student loans than students who dropped out of all colleges (most of which are not-for-profit).

These graduates defaulted on their student loans 19.2% of the time–still more often than the average college student who dropped out.

For-profit college students struggle to find jobs

Why are for-profit college dropouts and graduates more at risk of defaulting on their student loans? These colleges are often more expensive, forcing students to take out large private loans to cover costs.

And most private loans don’t have the sort of favorable terms that federal student loans do. They often come with higher interest rates and aren’t eligible for alternative federal repayment programs like Income-Based Repayment, which can help students lower their student loan payments based on their income.

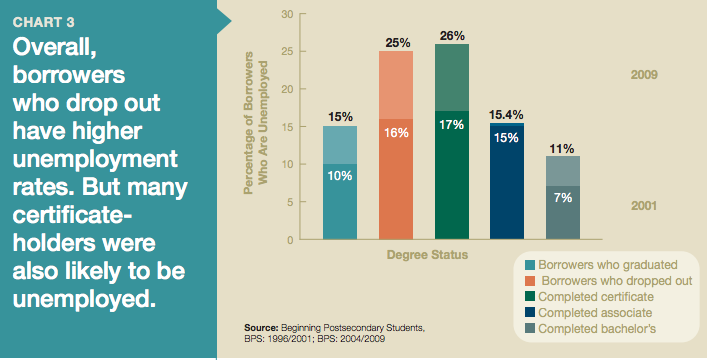

Besides having loans are often harder to pay off and greater balances than not-for-profit college borrowers, those who drop out or graduate with just certificates are more likely to be unemployed, making it difficult to afford monthly student loan payments.

This adds to their risk of falling behind on their student loan payments and going into default.

Student loan borrowers who drop out have the highest unemployment rates, followed by those who graduate with just a certificate.

The dangers of student loan default

As we’ve written before, if you’re borrowing student loans, you should attempt to avoid default at all costs.

Otherwise, you could face some dire consequences, such as damaged credit and having your wages garnished.

To reduce your risk of defaulting on your student loans, we advise against attending most for-profit colleges, which have been criticized for leaving students with high debt and low chances of employment. We also recommend maximizing your federal student loans before turning to private loans to pay for college.

And if you’re struggling to repay your student loans or are already in default, we can help you get on a better repayment schedule and manage your student debt.

Give us a call at 1-888-234-3907 or contact us using this form and we’ll let you know how we can help.

college loans, loan repayment, repayment, student debt, student loan default, student loan repayment, student loans