As the cost of college has risen, the burden of paying for it has fallen on students more than ever.

CNBC reports that college students are saving an average of $7,801, according to the second edition of the Allianz Tuition Insurance College Confidence Index.

That’s up 17% from $6,678 in 2017.

As college has gotten more expensive, more families have made it a priority to save money to put toward their children’s college education.

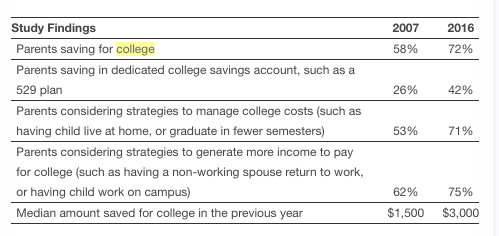

According to Fidelity Investments’ 10th Annual College Savings Indicator Study, as reported by GoodCall, the percentage of parents saving for college is at an all-time high.

There are many factors that determine financial aid eligibility, and it can be difficult to know how much aid you’ll get before you apply.

With college being such a large investment, it’s important to do research and understand how financial aid is determined before applying to colleges in order to maximize your financial aid package.

In a recent segment on Time Money, Lynnette Khalfani-Cox, author of College Secrets: How to Save Money, Cut College Costs and Graduate Debt Free, explains how to maximize your financial aid, the difference between merit and need-based aid, and why you should fill out the FAFSA even if you don’t think you’ll qualify for aid.

You thought you were doing the right thing by investing in a 529 plan to save for your child’s college. But what if your student receives a scholarship that covers most, if not all, of his or her college expenses?