It’s an age-old question that’s been debated by philosophers from Socrates to The Notorious B.I.G.: Does mo’ money equal mo’ problems? It just might, if that money is being taken out to pay for college. Graduates with student debt are less happy Many students and families think that attending a prestigious, well-known college is the […]

We’ve pledged our support for several of Senator Elizabeth Warren (D-MA)’s initiatives that would help reduce student debt, including her recent bill to let borrowers refinance their loans at lower rates.

Unfortunately, today our hopes were dashed by the news that Senate Republicans had blocked Sen. Warren’s bill.

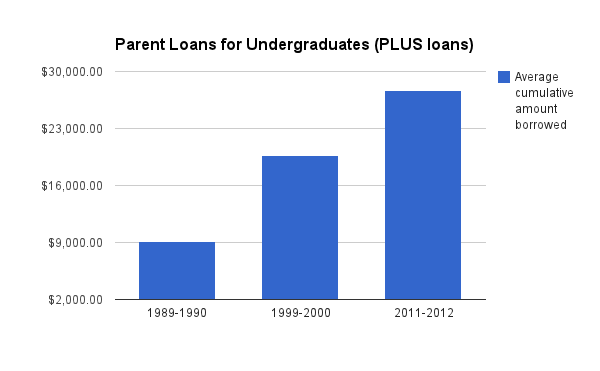

Students aren’t the only ones feeling the brunt of the student debt crisis: their parents are as well.

The latest figures from the National Center for Education Statistics showed that in 2011, 21% of parents took out Parent PLUS Loans to pay for their children’s college education. That’s a 60 percent jump from the year 1999, when just 13% of parents took out PLUS Loans.

And it’s not just that more parents are taking out loans for college: they’re taking out much larger loans as well. In 2011, PLUS Loan carried an average balance of $27,700 in inflation-adjusted dollars, up 40% from 1999, when the average balance was $19,700.

We’re proud to be based in Western New York, and we’re always glad to see the area get national recognition.

That’s why we were so excited to hear that Buffalo, the largest city in the region, was recently named the top medium-sized city for new college graduates by CreditDonkey.com.

The city’s low rents, low job competition and great nightlife make it an attractive destination for young college grads hungry for employment and fun while still affording their student loan payments.

It’s well-documented that student debt has grown rapidly over the past decade. The class of 2014 graduated with an average $33,000 in student loans per student, and the numbers will likely be event greater for next year’s class.

Given that student loan debt is increasing while salaries are declining, it’s not surprising that many young adults are struggling to accumulate wealth.

According to a new report from the Pew Research Center, it’s become increasingly difficult for young adults with student debt to save up enough money to buy a house, get married or start building their ‘nest egg.’

It’s official: the class of 2014 is the most indebted college class ever.

According to an analysis by Mark Kantrowitz published in the Wall Street Journal, the average 2014 college graduate has $33,000 in student loans, the most by any previous class.

Just a year ago, we were talking about how the class of 2013 was the most indebted class ever, but, as has been the case for the past 20 years, the record has been broken by this year’s class.

When you marry someone, you marry all of their baggage too–including their debt.

For younger Americans part of the generation graduating college with an average of $29,400 in student debt, the stakes are even greater. And for adults that go on to earn graduate, law, business or other advanced degrees, the student debt a spouse incurs could amount to hundreds of thousands of dollars.

It’s not the most romantic thing to think about, but in the case the couple ends up getting a divorce before paying all of their debt, dividing up the loans can be a tricky (and uncomfortable) prospect.

Sen. Elizabeth Warren (D-MA) says student loan interest rates are ‘crushing’ former students, and something needs to be done. She introduced a plan in March that would let student loan borrowers refinance their loans at lower interest rates. And last week, she filed the bill with the support of 27 co-sponsors. Plan would let borrowers refinance […]

President Obama unveiled the “Pay As You Earn” program in 2011 as a way to provide relief for student loan borrowers struggling to repay their loans. For student loan borrowers with low incomes, especially those in the public sector, the income-based repayment plan helps them manage their monthly payments even without a high-paying job.

The plan capped borrowers’ payments at 10% of their discretionary income per year. After 10 years, for the unpaid balances for those working in the public sector or for nonprofits would be forgiven, while private-sector workers’ debts would be wiped after a 20-year payment period.

But the program has had an unintended consequence: the government is taking on enormous debt, while colleges continue to raise tuition, having no incentive to lower costs when the government is footing the bill.

What’s keeping millennials up at night? It’s not just Netflix–it’s student debt.

NPR’s Morning Edition recently asked young adults, members of the millennial generation, what their biggest concerns were.

The results were telling: almost two-thirds responded that college debt was their biggest worry.