For recent college graduates, paying student loans can be a struggle.

But what if you could get yours paid for you just for moving to a certain city?

Niagara Falls, NY is trying to attract young residents by doing just that. The city will pay off $7,000 of a borrower’s student loans if they live in a designated area of the city for 2 years.

As we’ve explained, defaulting on your student loans has several consequences and could severely damage your credit score.

Of course, it’s best to avoid default by getting on the right student loan repayment plan for your situation and paying your loans on time. But if you’ve already defaulted on your loans, there is a way out.

This helpful video from Centsible Student explains what to do if you’ve defaulted on your loans and what options you have, including repayment plans and student loan consolidation.

We’ve written a lot about the great, affordable colleges in our home state of New York.

And beginning this year, prospective college students and graduates may have another reason to consider making a move to the Empire State: free student loan payments for two years.

If you have a lot of student loan debt, you’re far from alone.

Unpaid federal student loan debt is nearly $1.1 trillion, according to the latest data from the Consumer Financial Protection Bureau. And that’s not even counting private loans.

To show how great of a number that is, Debt.com put together an infographic of all of the things you could buy with $1 trillion.

With the national student debt topping $1 trillion, more students than ever are defaulting on their student loans.

The average student loan default rate is currently at 9.1%–that’s almost 1 in 10 borrowers.

If you have high student debt, you may be thinking, what’s the worst that can happen if you don’t pay it back?

A lot of terrible things, actually. From a severely low credit score to having your wages garnished, the consequences of defaulting on your student loans are dire.

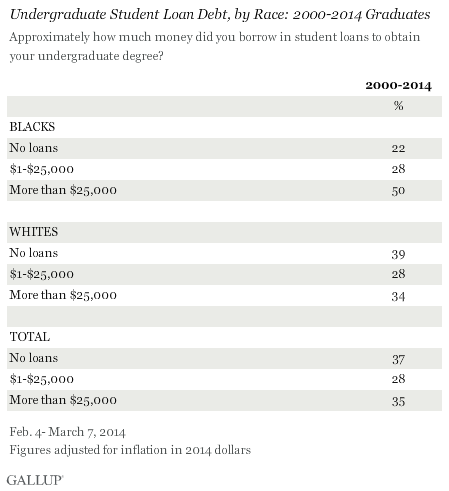

While student loan debt is a problem for most college graduates, it’s hitting one group significantly harder: black students.

A new analysis from Gallup found a significantly greater percentage of black college graduates carry student debt as compared to white students. Seventy-eight percent of black students graduate college with student loan debt, compared to 61% of white students.

They’re also more apt to carry greater debt loads, with half of black students reporting they have more than $25,000 in student loan debt, compared to only 34% of white students.

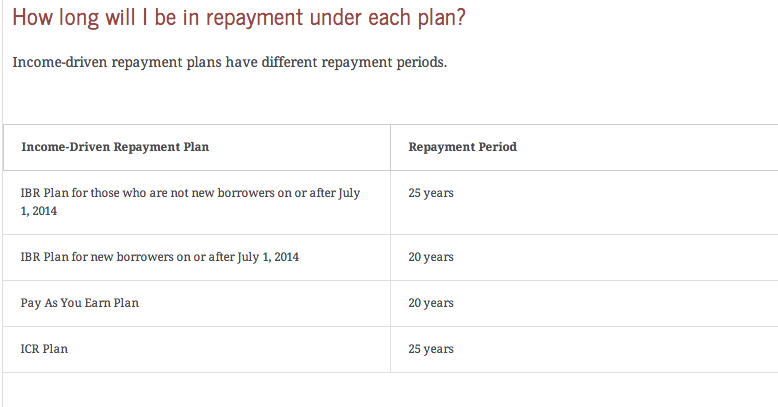

Student loan repayment can be extremely confusing for new graduates and their parents. With so many different plans and options, it can be difficult to figure out which one is best for you.

US News recently published a helpful breakdown of the four student loan repayment plans that are income-driven, meaning that your payments are dependent on how much money you make.

With the average student debt load rising for college graduates, it’s not surprising that many parents feel obligated to help pay their kids’ student loans to prevent them from falling behind.

According to a survey of 5,000 Americans released Thursday by Citizens Financial Group, as reported by MarketWatch, 94% of parents of college students ages 18 to 24 say they think their personal burden for their kids’ college student loan debt is increasing.

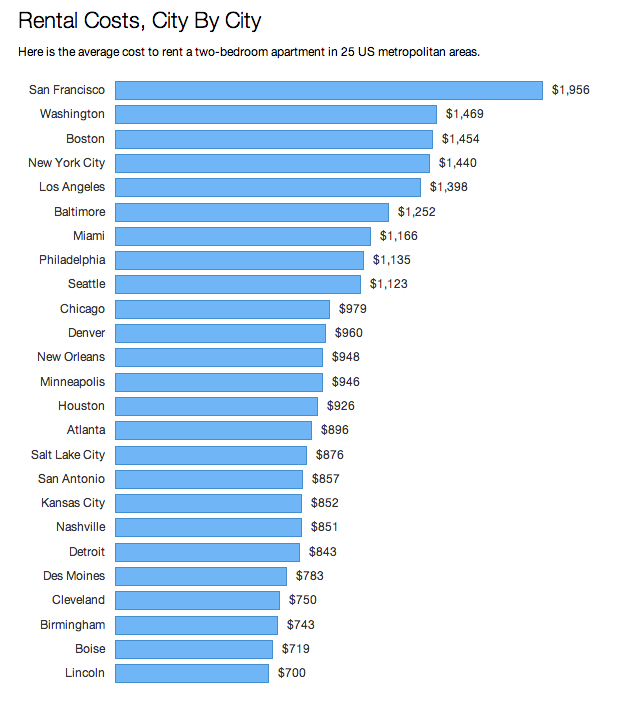

When many college students graduate, they’re tempted by the thought of moving to a big, exciting city.

Indeed, cities like New York and San Francisco provide many opportunities for work and play, so it’s unsurprising that they tend to attract hungry, eager young adults. But they’re also some of the most expensive cities in which to rent an apartment.

Many financial experts say you shouldn’t spend more than 30 percent of your income on housing, but for most graduates living in big cities, rent is their biggest expense. That’s why they often struggle to make other payments, like student loans.

When we say we are financial aid and student loan repayment consultants, many people assume we work for a college financial aid office, bank, or other outside organization.

But our work is completely independent. As student loan repayment consultants, we work one-on-one with student loan borrowers to set up a repayment schedule that allows them to manage their debt.