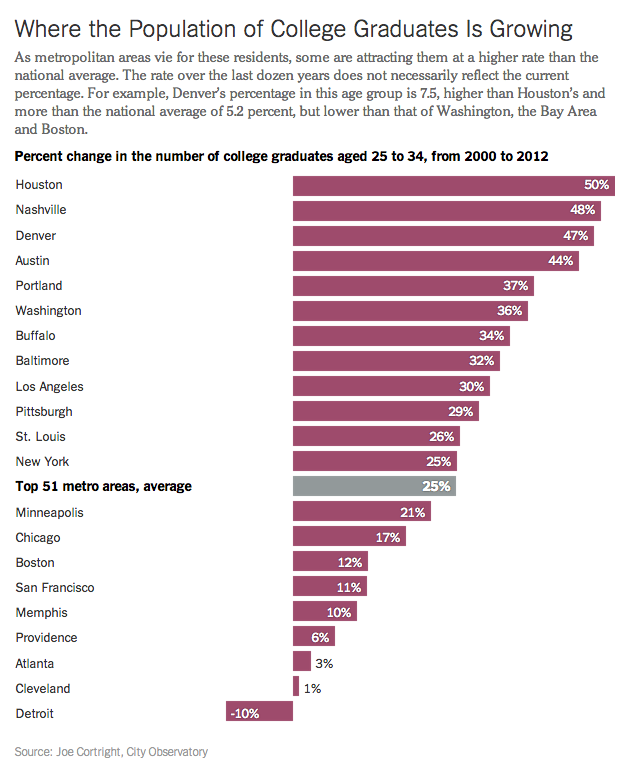

In the past, many young college graduates headed to big cities like New York, Boston and San Francisco in search of opportunities for work and fun.

Now, however, as more graduates have student debt to pay, many are flocking to up-and-coming cities like Pittsburgh and our hometown of Buffalo, which offer a great combination of good nightlife and a low cost of living, the New York Times reports.

Given the consistent rise in the cost of college over the past two decades, it’s no secret that student loan borrowing and student debt are at all-time highs.

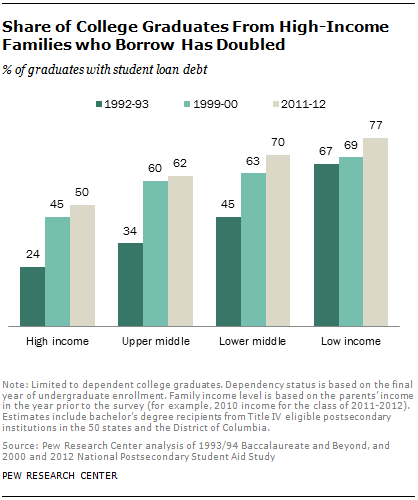

As you might expect, the percentage of students from low-income families who take out student loans to pay for college is greater than their higher-income counterparts, with 77% of low-income students borrowing for college in 2011-12 vs. 50% for high income students.

However, according to Pew Research Center, the rate at which students from more affluent families are borrowing is increasing faster than that at which low-income students are taking out student loans.

With the national student debt topping $1 trillion, more students than ever are defaulting on their student loans.

The average student loan default rate is currently at 9.1%–that’s almost 1 in 10 borrowers.

If you have high student debt, you may be thinking, what’s the worst that can happen if you don’t pay it back?

A lot of terrible things, actually. From a severely low credit score to having your wages garnished, the consequences of defaulting on your student loans are dire.

With the average student debt load rising for college graduates, it’s not surprising that many parents feel obligated to help pay their kids’ student loans to prevent them from falling behind.

According to a survey of 5,000 Americans released Thursday by Citizens Financial Group, as reported by MarketWatch, 94% of parents of college students ages 18 to 24 say they think their personal burden for their kids’ college student loan debt is increasing.

When we say we are financial aid and student loan repayment consultants, many people assume we work for a college financial aid office, bank, or other outside organization.

But our work is completely independent. As student loan repayment consultants, we work one-on-one with student loan borrowers to set up a repayment schedule that allows them to manage their debt.

Many of the nation’s top universities, such as Harvard, Stanford and Duke, are lauded for having need-blind admissions policies, meaning they don’t take into account a student’s ability to pay for college when making admissions decisions. These schools say the policy a way to make sure the best students are accepted because of their merit, […]

It’s an age-old question that’s been debated by philosophers from Socrates to The Notorious B.I.G.: Does mo’ money equal mo’ problems? It just might, if that money is being taken out to pay for college. Graduates with student debt are less happy Many students and families think that attending a prestigious, well-known college is the […]

Is a college degree worth the cost? Should everyone go to college? In the video below from CNN Money, “Freakomics” author and journalist Stephen Dubner answers these questions about higher education and offers his take on the rising cost of college. Dubner says that, overall, getting a college degree pays off over time. If, however, […]

It’s well-documented that student debt has grown rapidly over the past decade. The class of 2014 graduated with an average $33,000 in student loans per student, and the numbers will likely be event greater for next year’s class.

Given that student loan debt is increasing while salaries are declining, it’s not surprising that many young adults are struggling to accumulate wealth.

According to a new report from the Pew Research Center, it’s become increasingly difficult for young adults with student debt to save up enough money to buy a house, get married or start building their ‘nest egg.’

It’s official: the class of 2014 is the most indebted college class ever.

According to an analysis by Mark Kantrowitz published in the Wall Street Journal, the average 2014 college graduate has $33,000 in student loans, the most by any previous class.

Just a year ago, we were talking about how the class of 2013 was the most indebted class ever, but, as has been the case for the past 20 years, the record has been broken by this year’s class.